Overview

Many Australians use an adviser to manage their superannuation, investments and insurance. These people generally choose their adviser – someone they feel they can trust – and the adviser recommends a product that allows them to manage their client’s needs efficiently. These products, generally known as platforms, are built to give advisers ready access to the information they need.

But how do these platforms compare? Which platforms are stronger and in which areas?

For many years we have rated superannuation and pension products using criteria that assumes that members do not have a financial adviser, so the fund must offer strong core investments and helpful guidance direct to members to drive better outcomes. But when we rate platforms, we need to consider how the wider investment menu has been constructed and monitored, and how the platform helps advisers service their members efficiently to drive better outcomes. It is important to note that our platform ratings use different criteria than our super and pension product ratings and may produce different results when applied to particular platforms.

By applying our knowledge and experience of platforms, we compare them in a way that is both fair and rigorous, and on an 'apples with apples' basis.

The result is a set of ratings that encapsulate our view about the quality of each platform we rate. We express those ratings in terms of Apples. Platforms earn a rating ranging from 5 Apples, our highest grade, to 1 Apple, our lowest. In practice, we don’t expect we will award any platforms with a rating of 1 or 2 Apples, as these platforms would not pass our initial screening process to identify quality platforms that we believe should receive a rating.

Our ratings are based on information that is either publicly available or is provided directly to us by the platforms themselves.

Chant West Platform Rating

5 Apple – Highly Recommended is the highest Chant West rating for a platform. To earn 5 apples, a platform must have scored highly across most of our key areas of assessment which include adviser services, investments, fees, client services and organisation.

4 Apple – Recommended is the second highest Chant West rating for a platform. To earn 4 apples, a platform must have scored highly across some of our key areas of assessment which include adviser services, investments, fees, client services and organisation.

3 Apple – Approved is the third highest Chant West rating for a platform. To earn 3 apples, a platform must have scored at least moderately across most of our key areas of assessment which include adviser services, investments, fees, client services and organisation, with areas of potential improvement identified.

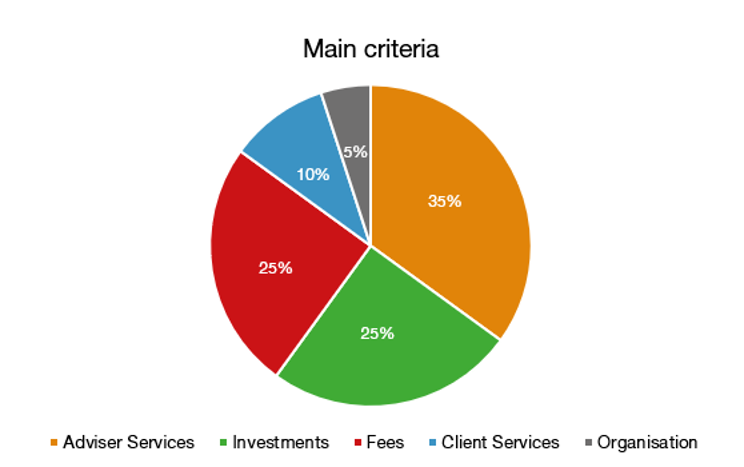

Main Criteria

In rating platforms, we apply a methodology that we have developed over the past 10 years of assessing platforms. This focuses on five main criteria: adviser services, investments, fees, member services and organisational strengths.

We determine a score for each of the main criteria and then weight these to provide an overall rating for the platform. The chart below shows the main criteria we use and the weights we assign to them.

Adviser Services

We consider adviser services as the most important part of a platform’s offering. The benefit of a platform is that it offers great efficiencies to advisers to enable them to focus on providing strategic advice for their clients, rather than spending their time on platform administration. This is an important contributor to providing strong member outcomes for platform clients. Adviser services accounts for 35% of our overall platform rating.

When we rate a platform’s adviser services, we consider the full range of services offered to advisers. We assess the Adviser Online portal, focusing on the process for buying and selling assets, business level reporting across the adviser’s client base, and reporting on individual client accounts. We also assess the tools provided for advisers to efficiently manage their client’s cash as well as data feeds from various financial planning software packages.

We also consider how the platform makes it easy for clients to provide consent on various actions where required, such as applications, buy/sell transactions, fee consents and corporate actions. This includes digital consent functionality, the range of digital signature solutions and online identification solutions.

And we consider the support provided to advisers through the contact centre, technical support and practice management to help them service their clients more effectively.

Investments

Investments are obviously an important part of a platform as they are the means through which long-term value is generated for clients. Investments account for 25% of our overall platform rating.

When we rate a platform’s investments, we do not assess every investment option that is available but rather the range of investment options offered including managed funds, SMAs, listed securities, term deposits and longevity products. We also look closely at the flexibility of the SMA and share trading structure to meet the needs of each licensee, adviser and client. We also assess the quality of the platform’s investment governance, including the process for approving and monitoring investments on the platform.

Fees

The fees a platform client pays – either directly from their account or indirectly through their investments – have a bearing on how much money they have in retirement.

When we assess a platform on fees, we look at a range of scenarios covering different balances across super, pension and IDPS, considering both full menu offerings and core menu offerings. We also consider account linking scenarios that provide benefits to clients when they are part of a family group. Where meaningful discounts are provided, we also take into account the average fee discounts provided to a platform’s client base. And we also consider the interest paid on the cash account, investment fee rebates and the disclosure of investment fees by the platform.

Fees account for 15% of our overall rating.

Client Services

While platforms are built for advisers to manage their clients efficiently, we cannot forget that the end customer is the client. We expect platforms to provide a range of services to help clients understand their investments, all in the context of these clients having an adviser to lead them.

The client services we consider includes the client portal and member app which both provide snapshots of a client’s investments, and also include a range of reports that can be run for clients who want further information on their account. We also consider the effectiveness of the annual client statement in clearly showing clients how much they have and how it is invested, as well as any client-friendly reports that the adviser can run from the adviser portal to share with their client. We also consider the retail insurance offering as part of the client services.

Client services accounts for 10% of our overall weighting.

Organisation

It is important to know that the platform has the strength and resources to continue to provide positive outcomes for clients and their advisers over the longer term.

When we assess a fund on organisation strengths, we look at who owns or controls it, its capital backing and profitability, ongoing investment in the platform, its scale and net flows, as well as how widely it is used by advisers. Organisation accounts for 5% of the overall rating.

Process

Chant West conducts annual meetings with each platform covering all the components of the rating. Each meeting typically lasts between 3 and 4 hours. At least two Chant West Research staff attend all meetings.

To determine the quality and effectiveness of a platform’s adviser and client member services, we request that each rated fund provides a range of documents that includes (but is not limited to):

- Snapshots of adviser portal screens

- Snapshots of client app and client portal screens

- Investment governance documentation

- Information on average fee discounts to clients

Disclaimer: ©Zenith CW Pty Ltd ABN 20 639 121 403 (Chant West), Authorised Representative of Zenith Investment Partners Pty Ltd ABN 27 103 132 672, AFSL 226872 under AFS Representative Number 1280401, 2023. This website is only intended for use by Australian residents and is subject to use in accordance with Chant West’s Terms of Use and should be read with Chant West’s Financial Services Guide. Products, reports, ratings (Information) are based on data which may be sourced from a third party and may not contain all the information required to evaluate the nominated product providers, you are responsible for obtaining further information as required. To the extent that any Information provided is advice, it is General Advice (s766B Corporations Act). Individuals should seek their own independent financial advice and consider the appropriateness of any financial product in light of their own circumstances and needs before making any investment decision. Chant West has not taken into account the objectives, financial situation or needs of any specific person who may access or use the Information provided including target markets of financial products, where applicable. It is not a specific recommendation to purchase, sell or hold any product(s) and is subject to change at any time without prior notice. Individuals should consider the appropriateness of any advice in light of their own objectives, financial situations or needs and should obtain a copy of and consider any relevant PDS or offer document before making any decision. Information is provided in good faith and is believed to be accurate, however, no representation, warranty or undertaking is provided in relation to the accuracy or completeness of the Information. Information provided is subject to copyright and may not be reproduced, modified or distributed without the consent of the copyright owner. Except for any liability which cannot be excluded, Chant West does not accept any liability whether direct or indirect, arising from use of the Information. Past performance is not an indication of future performance. Chant West ratings and research are prepared by Chant West and are not connected in any way to research and ratings prepared by any of our related entities.