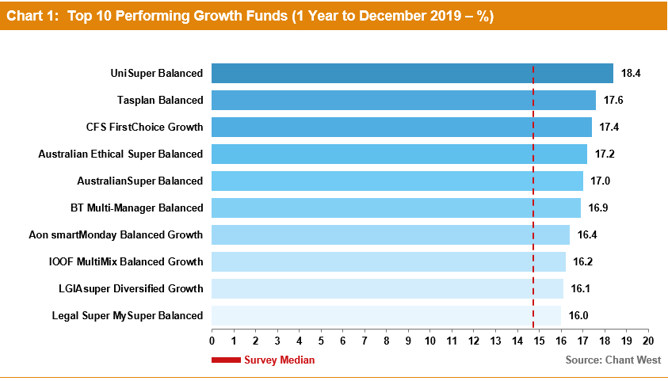

Super funds put in an outstanding performance in 2019, with the median growth fund up 14.7%. This was the best calendar year return since 2013 and the seventh best in the entire 27½ year history of compulsory superannuation. UniSuper Balanced took out top spot with a lofty return of 18.4%. Even the worst performer in our growth category returned a healthy 10.5%, which was nearly 9% above the rate of inflation. Growth funds are those that have a 61 to 80% allocation to growth assets and are the ones in which the majority of Australians are invested.

Chant West senior investment manager Mano Mohankumar says: "Very few would have predicted such a strong result 12 months ago when growth funds had just lost 4.6% over the December 2018 quarter and investor sentiment was decidedly negative. The 14.7% return represents the eighth straight positive year, and the 10th out of the past eleven.

"The 2019 result brings the average return over the past 10 years to 7.9% per annum. That's a tremendous run, but we should remember that it partly represents the recovery from the GFC when the median growth fund fell about 26%. We also need to keep in mind that growth funds aren’t designed to yield such returns over the long term – typically they're built to return 3.5% above inflation per annum which translates to 5.5% to 6% per annum over the long term, or rather less than that in today's low inflation environment. So it would be a mistake to assume that the level of returns over the past decade will continue. At some stage they’re going to revert to more ‘normal’ levels, and there will be more challenging times ahead.

"Shares remain the main contributors to growth fund performance with about a 53% allocation on average. But today's funds are well-diversified across a range of other assets as well, and in 2019 all asset sectors delivered positive returns. The better performing funds were generally those that maintained higher allocations to listed shares, which had a terrific year. International shares surged 27.4% in hedged terms and 28% unhedged while Australian shares gained 23.8%. Funds would also have benefited greatly from having money invested in listed real assets with global listed infrastructure, global listed property and Australian listed property returning 24.2%, 21.2% and 19.6%, respectively. Those that kept more of their traditional defensive exposure in bonds rather than cash would also have helped their performance."

Chart 1 shows the year's top 10 performing growth options over the 2019 calendar year.

Notes:

Notes:1. Where a super fund has more than one investment option in the Growth category, only its main investment option has been included in the top 10.

2. Performance is shown net of investment fees and tax. It is before administration fees and adviser commissions.

Other key content:

- Diversified fund performance by risk category (page 2)

- Top 10 performing growth funds over 10 years (page 2)

- Retail lifecycle product performance (page 3)

- Long-term performance including rolling 5 year returns chart (page 4)

- Risk objectives and calendar year by year performance chart (page 5)

- Asset sector performance (page 6)

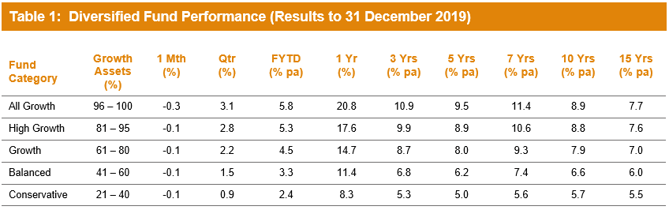

Table 1 compares the median performance for each fund category in Chant West's Multi-Manager Survey, ranging from All Growth to Conservative. Over every period shown, all risk categories have met their typical long-term return objectives, which range from CPI + 2% for Conservative funds to CPI + 4.75% for All Growth.

Note: Performance is shown net of investment fees and tax. It is before administration fees and adviser commissions.

Source: Chant West

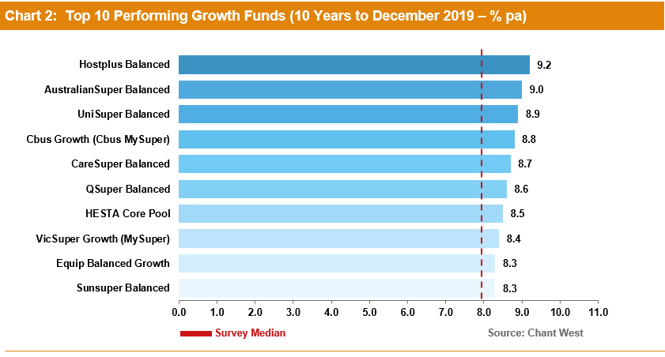

Chart 2 shows the top 10 performing growth options over 10 years.

Notes:

1. Where a super fund has more than one investment option in the Growth category, only its main investment option has been included in the top 10.

2. Performance is shown net of investment fees and tax. It is before administration fees and adviser commissions.

Lifecycle Funds Operating As Designed

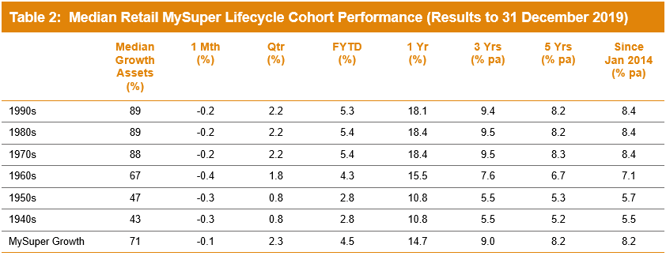

Mohankumar says: "While our Growth category is still where most people have their super, a meaningful number are now in so-called 'lifecycle' products. Most retail funds have adopted a lifecycle design for their MySuper defaults, where members are allocated to an age-based option that is progressively de-risked as that cohort gets older.

"It's difficult to make direct comparisons of the performance of these age-based options with the traditional options that are based on a single risk category, and for that reason we report them separately. Table 2 shows the median performance for each of the retail age cohorts, together with their current median allocation to growth assets."

Notes:

1. Performance is shown net of investment fees and tax. It is before administration fees and adviser commissions.

2. January 2014 represents the introduction of MySuper.

Source: Chant West

While lifecycle is the most common MySuper default in the retail sector, most not-for-profit funds still use their traditional growth options for that default role. A few have gone down the lifecycle path, however, and while the general premise is the same the way it is implemented is different. Rather than allocating members to age-based cohorts as retail funds do, in the not-for-profit lifecycle model members typically ‘switch’ from one traditional risk category to another at particular ages. The diversified options that underlie these strategies are included in Table 1.

To help illustrate the early results of the retail lifecycle model, Table 2 includes a row for traditional MySuper Growth options – mainly, but not all, not-for-profit funds. Care should be taken when comparing the performance of the retail lifecycle cohorts with the median MySuper Growth option, however, as they are managed differently so their level of risk varies over time.

We have generally seen strong performance from growth assets in recent years so, as we would expect, the options that have higher allocations to growth assets have generally done best. Younger members of retail lifecycle products – those born in the 1970s, 1980s and 1990s – finished the 2019 calendar year well ahead of the median MySuper Growth fund on average, and have generally held their own over the longer-term. However, they have done so by taking on more share market risk. The 1960s funds are in the de-risking phase, so their growth asset exposure is lower than that of the median MySuper Growth fund. Nevertheless, this age cohort has outperformed the MySuper Growth median over the past year. This is because the 1960s funds' growth asset exposure is mainly in the form of listed shares and REITs with less invested in unlisted and alternative assets to which the not-for-profit MySuper Growth funds have meaningful exposures. However, the 1960s funds are still behind the median MySuper Growth fund over the longer-term.

The older age cohorts (those born in the 1950s or earlier) are less exposed to share market risk. Capital preservation is more important at those ages so, while they miss out on the full benefit in rising markets, older members in retail lifecycle options should be better protected in the event of a market downturn.

Funds Still Delivering On Long-Term Targets

While 2019 was a tremendous year, Mohankumar reminds fund members to think long term. "Certainly look at what your fund delivered over the year, but it’s even more important to know what its long-term objectives are and whether it's achieving them. Most growth funds aim to beat inflation by 3% to 4% a year. We now have data going back 27½ years to July 1992, the start of compulsory super. Over that period, the annualised return is 8.3% and the annual CPI increase is 2.4%, giving a real return of 5.9% per annum – well above that 3% to 4% target. Even removing the particularly strong years from the early to mid-1990s as we came out of recession and looking at the past 20 years, super funds have returned 6.9% per annum – 4.3% above inflation. Let's not forget that the 20 year return still includes two sharemarket downturns – the 'tech wreck' and the GFC.

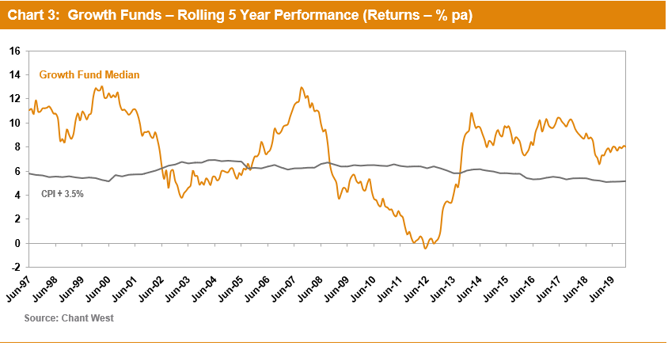

"The strong long-term performance is borne out visually in Chart 3, which compares the growth category median with the average return objective of CPI plus 3.5% per annum over rolling five year periods – that's after investment fees and tax. Until 2009, the median fund outperformed the target most of the time. The GFC brought that to an abrupt halt, and the median dipped below the target line for several years. Now, with the GFC period out of the calculation, the five year return has been tracking well above the target line for about six-and-a-half years."

Note: The CPI figure for the December 2019 quarter is an estimate.

Returns Are Important But Risk Matters Too

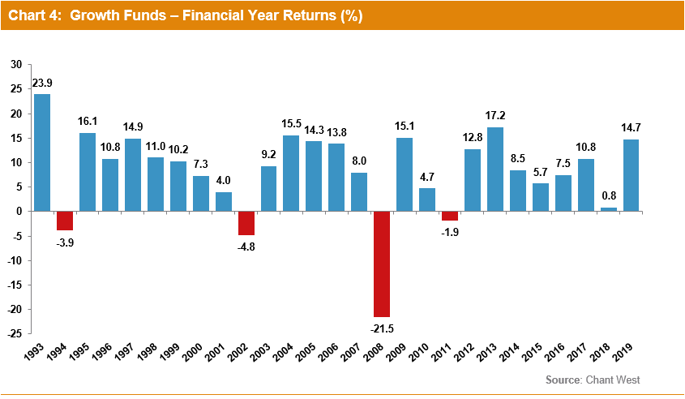

Mohankumar says: "Returns are important but so is risk, and most funds also set themselves a risk objective. Risk is normally expressed as the likelihood of a negative annual return, and typically a growth fund would aim to post no more than one negative return in five years on average. Chart 4 plots the year by year performance of the median growth fund over the 27 full calendar years since the introduction of compulsory super. The objective would be no more than five negative years in that time. As it turns out there have only been four, so the risk objective has been met as well as the performance objective.

"Over the longest period we can measure Australia's major super funds have delivered on their promises to members, growing their wealth in real terms while protecting them from undue risk. That's a great achievement, and it's an important message their members should be aware of, too."

The Investments That Drove The Performance

While there are differences between funds' investment strategies, even within the same risk category, most of their performance is driven by what happens in the major investment markets.

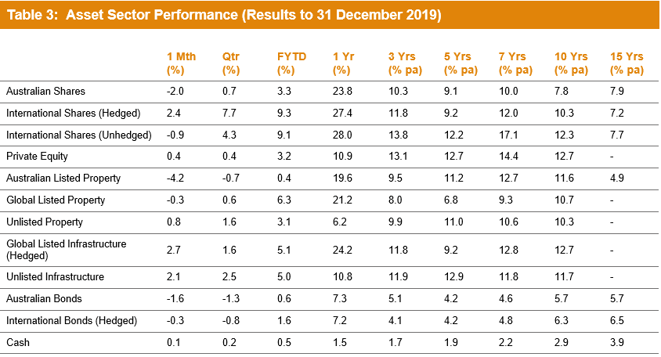

Table 3 shows the performance of all the main asset sectors over different time periods to the end of December 2019. We have used market indices for all sectors other than private equity. For this sector, we have used the returns of a major fund in our survey that are representative of those markets.

Source: Chant West

The Key Points To Note For The 2019 Calendar Year Are:

- International shares was the strongest performing asset sector returning 27.4% in hedged terms and 28% unhedged.

- Australian shares also had a tremendous year, gaining 23.8%.

- Australian listed property had a great year, returning 19.6% while global listed property returned 21.2%. Unlisted property returned a more modest 6.2% after a strong run in prior years.

- Global listed infrastructure was one of the best performing asset sectors with a return 24.2%. Meanwhile, unlisted infrastructure and private equity, while not quite at the heights of some recent years, had another solid year, up 10.8% and 10.9%, respectively.

- In the traditional defensive asset sectors, bonds had a good year with Australian bonds up 7.3% and global bonds almost matching that at 7.2%. With interest rates at an all-time low, it's not surprising that cash was the worst performing sector with a return of just 1.5%.