the complexities of negative screening in responsible investing. Learn how to balance transparency, regulatory demands, and investor expectations to create robust and ethical investment strategies.

Responsible investing, like all investment philosophies, is influenced by market sentiment and performance. One of the challenges is that, unlike traditional investment strategies, responsible investing is often geared heavily toward personal values. Nowhere is this more strongly expressed than in negative screening. While it’s only one of the several strategies that make up responsible investing, it remains one of the most popular. Unfortunately for managers both in and outside super, it’s also one of the most dangerous areas in which to express an investment thesis, given its highly scrutinised.

Negative screening is far from straightforward. It involves more than just excluding issues, it requires nuanced and dynamic management. This is further compounded by two issues. A regulatory regime that rightly focuses on transparency from managers to prevent greenwashing and a diverse pool of individual investors whose views on what the ‘right’ issue to avoid is as varied as the individuals involved.

Balancing simplicity and clarity

Negative screening has long been used to avoid companies involved in controversial activities. However, increasing regulatory attention on greenwashing allegations complicates this process. Typically, this is not because funds are trying to hide the details, it’s because from a promotional perspective, explaining the details that negative screens are governed by isn’t always simple. Screens often rely on a complex set of rules and applicable thresholds. The challenge for managers is balancing simplicity with transparency.

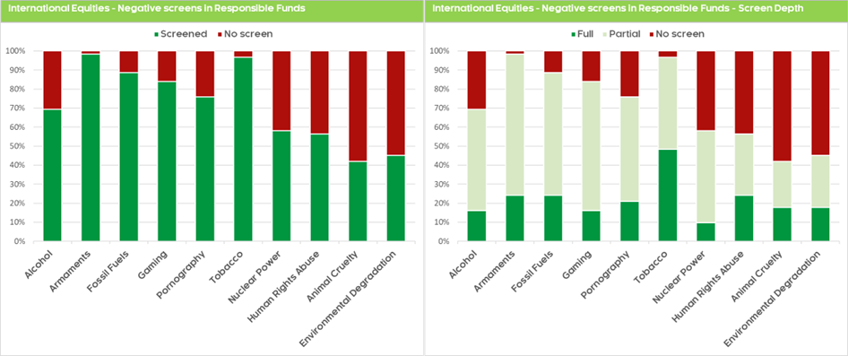

Screens are usually not absolute. In international equities funds, for example, Zenith’s cohort of responsible funds use screens on key issues (chart on the left). However, if we segregate these screens into those that ‘fully’ screen for an issue versus using materiality thresholds (partial screens), the picture looks very different (chart on right). While nearly 70% of these funds screen on alcohol, around 55% have some form of materiality threshold associated with it.

Source: Zenith Investment Partners. Data based on Zenith Approved Product List at 30 April 2024.

Why complex rules?

Business activities are interconnected and don’t happen in isolation, boundaries need to be drawn somewhere. The extent of activities also needs to be considered in the context of both their supply and value chains.

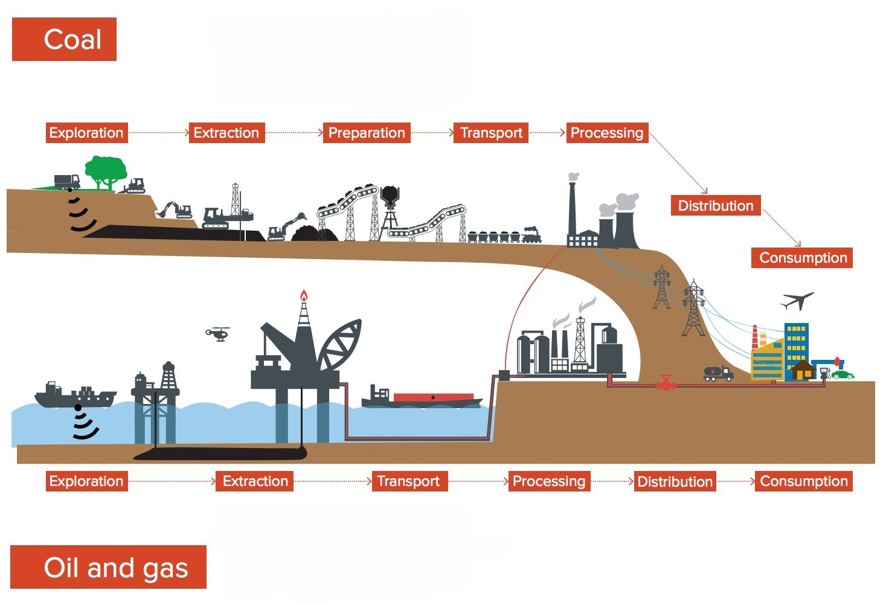

For example, fossil fuels are a common screen in responsible investing. The many stages involved in fossil fuel production (as illustrated below), complicate decisions about where screens should begin and end.

Stages and sectors of fossil fuel production and consumption

Source: Runkel, M., Trilling, M. et al.

For example, while many funds have screens dealing with coal, it is not uncommon for these to still permit exposure to companies which generate revenue from coal exploration and/or refining. Similarly, while others may apply screens regarding thermal coal, metallurgical coal (for steel making) may still be permitted. And what about customers? Should those involved in transport or distribution be considered? What about heavy consumers like airlines?

Looking at other controversial industries, there are further complexities. Weapons for example. Do you just limit controversial types and their manufacturers? What about component suppliers? Raw materials? Drawing the line is complex and multi-faceted.

The role of materiality thresholds

But why use materiality thresholds? In essence, it’s because eliminating exposures can be complicated when managing funds. Issues can include:

Non-disclosure: Companies often don’t disclose ‘immaterial’ revenue lines below thresholds based on financial reporting standards. These are often levels such as 5% of profit before tax or 2-3% of operating income. Accordingly, you can be caught out by an extremely minor undisclosed revenue stream.

Indirect exposure: Controversial exposures may occur in the supply or value chain rather than in direct operations and as such usually not reported. But if some data aggregators considered indirect involvements cause for concern, having a 0% threshold could trigger a breach.

Mergers & acquisitions: Companies may acquire businesses that generate minor revenues from excluded activities. If a 0% threshold was applied, it would either be a breach or at least trigger an immediate sale. But what if the company planned to divest the offending activity in the new entity? Minimum thresholds allow time to review and plan a course of action.

Lagged data: Company reporting is backward-looking. Fund managers usually find that creating a materiality threshold allows leeway to accommodate changes in activity that will only become apparent after the fact and prevent an inadvertent exposure breach.

Fund disclosures: Given the legal obligations in fund offer documents, the issuers need to avoid potential accusations regarding misleading or deceptive behaviour in disclosures. Having a 0% exposure threshold is likely to be troublesome given any minor infringement could trigger enforcement and litigation.

Avoidance vs engagement: Avoidance (or divestment) as a change agent may have limited effectiveness and real-world impact within the timeframes sought by many managers. Some may prefer to rely on holding and engaging with some companies as a way to transition away from undesirable activities.

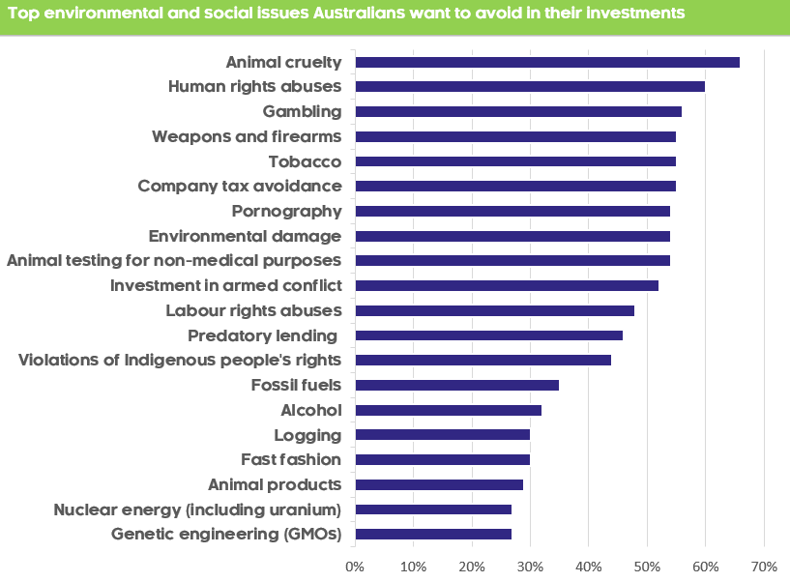

The subjectivity of materiality

Financial materiality represents the point at which an error or omission could influence the users' decision-making regarding financial statements. Materiality is generally subjective and varies depending on size, location, and circumstance. But with screening, what’s viewed as ‘right’, let alone material, is often in the eye of the beholder. Investor concerns are dynamic and span a wide range of issues, as shown on the following chart.

Source: Responsible Investment Association of Australasia (RIAA), From Values to Riches 2024

Increasingly, fund managers and financial advisers are being challenged by clients on negative screens. For ethically motivated investors, the fine print of materiality can be contentious. Unlike dealing with regulators around clarity and transparency, addressing investors’ greenwashing requires a different approach. Perhaps, rather than simply itemising what screens cover, conversations need to be had on why they don’t cover some aspects and how that relates to the investment strategy. Some points might include:

- Given the risks in contravening a screen, thresholds are there to ensure robustness rather than perfection;

- Thresholds can limit excessive alteration to the size of the investable universe which might work against other fund objectives (e.g. sector biases, investment style, and returns targets); and;

- Just as company activities are dynamic, so too are views on materiality and controversy issues. Appropriate thresholds provide leeway to manage changing circumstances.

Negative screening serves a valuable purpose for investors sensitive to controversial issues. However, a fund’s screening criteria are unlikely to accommodate all investor preferences perfectly. The challenge is to understand the purpose of a screen’s design and how that in turn serves the purpose of the fund’s overall strategy.