Super funds were back in positive territory in October, with the median growth fund (61 to 80% in growth assets) up 0.5% for the month. With six positive returns in the past seven months, and with what we’ve seen so far in November, the median growth fund has a good chance of finishing the 2020 calendar year in positive territory.

Chant West senior investment research manager Mano Mohankumar says: "The positive return in October was largely due to the performance of Australian shares, which returned 1.9%. International shares, however, headed in the opposite direction due to uncertainty around the US election and surging COVID cases, particularly in the US and Europe. International shares retreated 3.2% in hedged terms, but the depreciation of the Australian dollar (down from US$0.72 to US$0.70) limited that loss to 1.1% in unhedged terms. On average, funds currently have about 70% of their international shares exposure unhedged, and that foreign currency exposure provides a natural buffer against share market falls, as we saw in October.

"November has been extremely positive for markets so far. Joe Biden's election victory has removed much of the uncertainty that was weighing on share markets, although President Trump seems set on making the transition a difficult one. Additionally, last week pharmaceutical company, Pfizer, and biotechnology company, BioNTech, announced that they have developed vaccines that in testing was more than 90% effective in preventing COVID-19. While there is still a way to go before the trial is complete, share markets around the world have reacted euphorically. We estimate that the median growth fund is up over 4.5% for the month to date and up a remarkable 14% since the end of March, more than erasing the 12% loss experienced back in February and March. So with just over six weeks of 2020 remaining, we estimate that the median growth fund is up over 2% for the calendar year to date.

"Back at home, all states now have COVID numbers under control – although occasional outbreaks must still be expected. The share market has reacted positively to that news, and to progress reports on several potential vaccines that should become available in 2021. Earlier this month the RBA announced a package of measures to support job creation and the post-COVID economic recovery. This included lowering the official cash rate to a new all-time low of 0.1% and a quantitative easing program which will see the bank purchase $100 billion of government bonds over the next six months."

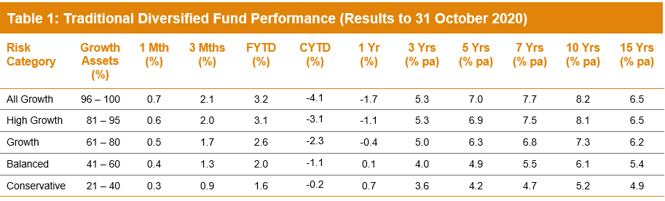

Table 1 compares the median performance for each of the traditional diversified risk categories in Chant West's Multi-Manager Survey, ranging from All Growth to Conservative. Over 5, 7, 10 and 15 years, all risk categories have met their typical long-term return objectives, which range from CPI + 2% for Conservative funds to CPI + 4.25% for All Growth.

Note: Performance is shown net of investment fees and tax. It is before administration fees and adviser commissions.

Source: Chant West

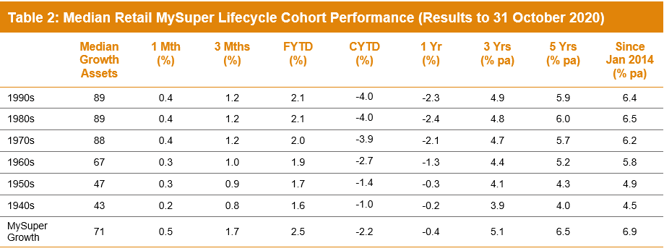

Lifecycle products behaving as expected

Mohankumar says: "While our Growth category is still where most people have their super invested, a meaningful number are now in so-called ‘lifecycle’ products. Most retail funds have adopted a lifecycle design for their MySuper defaults, where members are allocated to an age-based option that is progressively de-risked as that cohort gets older."

It’s difficult to make direct comparisons of the performance of these age-based options with the traditional options that are based on a single risk category, and for that reason we report them separately. Table 2 shows the median performance for each of the retail age cohorts, together with their current median allocation to growth assets. It also includes a row for traditional MySuper Growth options for comparison – nearly all of which are not-for-profit funds. Care should be taken when comparing the performance of the retail lifecycle cohorts with the median MySuper Growth option, however, as they are managed differently so their level of risk varies over time.

Notes:

1. Performance is shown net of investment fees and tax. It is before administration fees and adviser commissions.

2. January 2014 represents the introduction of MySuper.

Source: Chant West

Despite the strong recovery since April, the initial COVID-related setback in February and March is still being reflected in some of the shorter-term numbers, so those options that have higher allocations to growth assets have performed slightly worse over the past year. Over longer periods those higher-risk options, which cover the younger cohorts born in the 1960s or later, have generally performed better. However, despite taking on more share market risk, these younger cohorts haven’t performed as well as the median MySuper Growth option, over all periods shown.

The reason these younger cohorts in retail lifecycle funds have underperformed the MySuper Growth option over longer periods is that these funds, while generally well-diversified, still don't have the same level of diversification as many of the not-for-profit funds. This is mainly due to the not-for-profit funds' higher allocations to unlisted assets (unlisted property, unlisted infrastructure and private equity) – about 21% on average. This compares with the retail lifecycle fund average of 5% for these younger cohorts, although there are a few that have 10-14% unlisted asset allocations. These assets have been proven to add value over the long term, not just for their diversification qualities but also because they generate an illiquidity premium in their returns relative to listed markets. Such assets of course need to be managed carefully to ensure that enough liquidity is available when required, such as earlier this year. The liquidity of the vast majority of super funds held up remarkably well during the period that showed heightened demand for liquidity from early release, switching to cash and FX hedging settlements.

The older cohorts (those born in the 1950s or earlier) are relatively less exposed to growth assets so you would expect them to underperform the MySuper Growth median over longer periods. Capital preservation is more important at those ages so, while they miss out on the full benefit in rising markets, older members in retail lifecycle options are better protected in the event of a market downturn.

Long-term performance remains above target

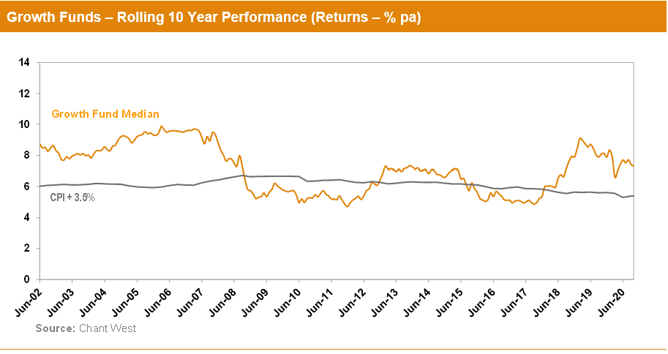

MySuper products have only been operating for less than seven years, so when considering performance, it is important to remember that super is a much longer-term proposition. Since the introduction of compulsory super in 1992, the median growth fund has returned 8% per annum. The annual CPI increase over the same period is 2.4%, giving a real return of 5.6% per annum – well above the typical 3.5% target. Even looking at the past 20 years, which now includes three share major market downturns – the 'tech wreck' in 2001–2003, the GFC in 2007–2009 and now COVID-19 – the median growth fund has returned 6.3% per annum, which is still ahead of the typical return objective.

The chart below shows that, for the majority of the time, the median growth fund has exceeded its return objective over rolling ten-year periods, which is a commonly-used timeframe consistent with the long-term focus of super. The exceptions are two periods between mid-2008 and late-2017, when it fell behind. This is because of the devastating impact of the 16-month GFC period (end-October 2007 to end-February 2009) during which growth funds lost about 26% on average.

Note: The CPI figure for October 2020 is an estimate.

International share market returns in this media release are sourced from MSCI. This data is the property of MSCI. No use or distribution without written consent. Data provided “as is” without any warranties. MSCI assumes no liability for or in connection with the data. Product is not sponsored, endorsed, sold or promoted by MSCI. Please see complete MSCI disclaimer.